The world center for art and culture, France is home to many famous landmarks such as the Eiffel Tower, the Louvre, Notre Dame, and the Palace of Versailles. Its capital city is the world’s capital of fashion and it has more tourists than any other country in the entire world. On the other hand, when it comes to importing and exporting goods from/to France, customs and tax compliance may not be very glamorous but confusing, complex and heavy, especially in its overseas departments.

–

READ MORE: Get to Know Our HS Classification Engine

–

Officially, the French Republic is divided into regions, which are further subdivided into departments. The twelve mainland regions and the island of Corsica make up what’s known as Metropolitan France. Metropolitan France makes up 82% of the land and 96% of the population of France.

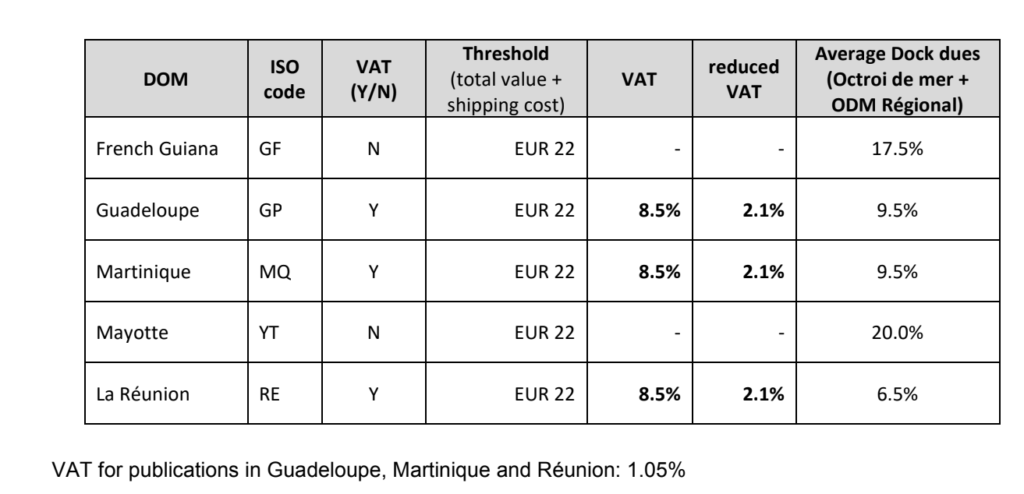

However, there are five remaining regions known as Departments d’Outre-mer or Overseas Departments, which are

- Guadeloupe

- Martinique

- French Guiana

- La Réunion

- Mayotte

These overseas departments form part of the European Union, as well as the Eurozone, meaning the Euro is their legal tender, however, their customs and tax rules differ a lot from France mainland.

Some overseas departments don’t charge VAT upon imports, for example. French Guiana and Mayotte have a 0% VAT rate for whatever geographical origin/destination is (EU or non-EU country). Customs duty has an additional tax named Dock Dues, which varies according to each specific region and governmental industry priorities.

Octroi de mer (Dock dues)

The French outermost regions are not part of EU customs territory for the purposes of VAT (Article 6 of the VAT Directive). To protect the local industry a century-old additional VAT scheme is in place, called Octroi de mer (Dockdues)

BtoC: Octroi de mer externe (ODM) = Octroi de mer + Octroi de mer régional (regional dock

dues)

BtoB: Octroi de mer interne = Octroi de mer + Octroi de mer régional (regional dock dues) In

order to simplify the obligations of small enterprises, tax exemptions or reductions should affect

all operators whose annual turnover is at least EUR 300 000. Operators whose annual turnover

is under that threshold should not be subject to dock dues; however, to balance this, they cannot

deduct the amount of that tax borne upstream.

More information can be found on https://ec.europa.eu/taxation_customs/turnover-taxes-french-overseas-departmentsoutermost-regions_en, published by the European Commission.

Sales Invoice

A sales invoice is mandatory for all shipments:

• For value < 300 DTS

- CN22 is mandatory

- Description of the goods should be also present on the CN22

- Commercial invoice inside the parcel

• For value > 300 DTS - CN23 is mandatory

- Description of the goods should be also present on the CN23

My Duty Collect has developed a suite of engines that accurately calculate all taxes and duties to all of the French overseas departments. If you are interested in learning more about our solution, subscribe to our blog and visit our website and LinkedIn page for more updates. You can also reach out to us by sending a message to info@mydutycollect.com. We will be happy to hear from you.